15 Healthcare Reforms to Live (Not Kill) For

If the US healthcare system were a patient, it would be sick, overweight, and due for major surgery.

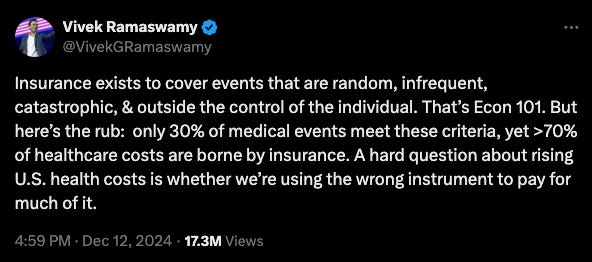

In my last installment about the ethics of healthcare vigilantism, I wrote:

Remember, though: the righteous, bloodthirsty chorus is the same group that offered thunderous applause at the passage of the Affordable Care Act (ACA). This law ignored every single fundamental reform needed to make healthcare more *affordable* and accessible.

The problem with the US healthcare system is not that there are eeeevil CEOs who deny people care. The problem is that it is a Care-tel—a corrupt orgy of providers, insurers, pharma, and politicians. This fantastic corporate-state circle jerk comes at our expense. If you’re gonna reform it, creating DMV-care For All is not the way. (Just ask a Brit or a Canadian.)

Instead, we must create a highly competitive, less corrupted, holistic healthcare ecosystem.

With that, I’ll cut to the chase. Here are 15 reform measures that needed to occur fifteen years ago.

Make it legal to buy health insurance across state lines. Insurance companies cartelize within states, making rate increases and lower quality more likely. For example, if your state has more coverage mandates, it’s probably less affordable. But with a national market—if United Healthcare sucks and gets a reputation for denying care, it would be legal to buy a policy from another state.

Expand the contribution limit for Health Savings Accounts (HSAs). The expense account effect plagues most of the US healthcare system. In other words, If someone else is paying for your blood test, you won’t care what they’re charging the risk pool. But premiums will go up. Making more patients as out-of-pocket purchasers means more health providers must compete for their dollars. This drives down costs.

Require care providers to post prices for all non-experimental procedures and treatments. It’s easier to be an effective price shopper when prices are easy to discover. If non-catastrophic costs come out of your HSA, you will care whether your blood test is $500 or $50. Again, the more people care about cost, the more competition lowers prices.

Offer poor people direct subsidies to expanded HSAs, replacing Medicaid. The government can offer the poor direct vouchers or tax credits. If people who use HSAs are incentivized to shop for better prices, those receiving means-tested assistance will be better price shoppers, too. HSAs can bear interest, which offers more incentives to compare prices as folks guard their tax-protected accounts. (Plus, eliminating Medicaid means eliminating fraud.)

Make insurance insurance again with catastrophic plans accompanying HSAs. Health insurance is supposed to cover significant, unanticipated health problems, not sniffles and stitches. Our third-party system should not function as pre-paid healthcare because that creates perverse incentives for abuse. Restrict insurance to serious injuries and diseases, and make smaller routine care out-of-HSA.

Decouple health insurance from employment by removing the tax advantage. Instead of giving employer-based insurance a tax advantage, which is an artifact of WWII policy, make all healthcare premiums and costs payable with pretax dollars. This will eliminate job lock by making all health insurance portable and drastically reduce overconsumption.

Make all coverage mandates, whether state or federal, 'mandate lite.' That means plans should prioritize flexibility, affordability, and minimal regulatory burden—requiring insurers to offer certain benefits but not force consumers to purchase them. This allows consumers to choose plans that align with their needs and budgets without being constrained by excessive coverage requirements that add to costs and encourage unnecessary use.

Eliminate community rating. Younger, poorer, healthier people should not have to pay the same premium as older, wealthier, sicker people. Community rating mandates create perverse incentives and unnecessarily high healthcare costs for the young. Relatively higher premiums based on actuarial science give older people more incentives to live healthier lifestyles.

Create national and state-based high-risk pools. Accessing affordable plans can be costly for people with preexisting conditions. High-risk pools create a system where 'guaranteed issue' regulations can remain in place. However, given their conditions, options for high-risk patients might be relatively more expensive, perhaps capped at no more than three times the standard premium. This cap ensures that coverage remains accessible while distributing costs more fairly across the risk pool.

Get rid of Obamacare’s marketplace. The ACA marketplace obscures the magnitude of subsidy and debt spending shouldered by taxpayers. It also preserves too many third-party payer distortions, such as overconsumption (the expense-account effect.) Indeed, don’t just get rid of Obamacare’s marketplace. Get rid of Obamacare entirely.

Eliminate Certificates of Need (CON) laws. These laws make it nearly impossible for a competitor to build a competitor clinic in a state because the competitor must get permission from politicians already bought by incumbents. Strike these corrupt, crony laws down once and for all.

Eliminate Medicaid. Rich retirees living in Palm Beach don’t need Medicaid, but many have paid into the system. By grandfathering in those who have paid, the rest of the population can graduate to a system in which the elderly poor go into an uncapped HSA + catastrophic plan system, which might also connect to high-risk pools. The HSAs can accumulate funds over many years rather than being pissed down the drain. Means-tested poor seniors can receive healthcare subsidies or tax credits to cover age-related rate increases.

Reform Big Pharma. Make it cheaper and easier to get safe drugs to market, but reduce the patent window for pharma companies and medical suppliers to hold patent monopolies through which they can jack up prices. I’ve got much more to say about reforming this industry, but I’ve run out of time.

Expand Health Insurance Mutuals and Legalize Healthcare Associations. Mutual insurance arrangements and healthcare associations are legal in the US, but regulatory hurdles at the state and federal levels make them difficult to establish. Significant deregulation, especially #1, would go a long way toward enabling mutuals and associations to develop along with innovative health plans, including those that incorporate healthy lifestyle incentives.

First, do no harm. Remove bureaucratic obstructions, destroy the Care-tel, unleash the innovators and entrepreneurs, and allow a competitive, accessible healthcare ecosystem to flourish wherever possible.

Remember,

Singapore, which has a patient-driven system (mixed market), only spends 2-3 percent of GDP on healthcare. Yet it has some of the world’s best health outcomes. By contrast, the US spends 17-18 percent of GDP—the world’s highest—on healthcare and cannot boast similar health outcomes.

Of course, Singaporeans walk more, drive less, eat healthier, and shoot each other less. Such factors have nothing to do with the healthcare system per se. Still, that Singaporeans can spend so little to get so much,

indicates a corrupt, rotten American system—a rigged game built by the politicians who have auctioned their souls to the Care-tel.

We have an unprecedented opportunity to make private, competitive healthcare affordable and accessible for all. But the Care-tel is still firmly in charge. I won’t hold my breath waiting for it to check itself into the reform clinic.

My follow-up conversation with ChatGPT resulted in:

1) What percentage of US healthcare expenditures are considered for routine care (as opposed to catastrophic care)?

Estimate: Approximately 40-50% of US healthcare expenditures are associated with routine care, while catastrophic care accounts for the remainder.

Routine care includes preventive services, regular check-ups, screenings, management of chronic conditions, and minor illnesses.

Catastrophic care includes high-cost treatments like trauma, surgeries, cancer care, ICU stays, and advanced procedures.

2) What percentage of routine care is paid through one's health insurance policy (as opposed to out-of-pocket or through one's HSA)?

Estimate: Approximately 70-80% of routine care costs are covered by insurance policies.

These costs include annual checkups, primary care visits, diagnostic tests, and screenings, often covered with minimal copays or deductibles.

The remainder is typically paid out-of-pocket or via HSAs. HSAs specifically cover a smaller share (~5-10%) due to their more selective use among Americans with high-deductible health plans (HDHPs).

3) If we were to reform US healthcare such that ALL routine care was paid out of an HSA or out of pocket, what sorts of cost savings could be realized for the system, including due to price competition?

Potential Cost Savings:

Administrative Simplification:

Routine care billing through insurance involves substantial overhead (e.g., claims processing, pre-authorizations, administrative staff). Paying directly could save an estimated 15-20% of routine care costs due to reduced administrative expenses.

Price Transparency and Competition:

Out-of-pocket payments would likely encourage price transparency and competition among providers, potentially lowering costs by an estimated 10-30%. For example:

Direct primary care clinics already show reduced costs compared to insurance-based pricing.

Providers would offer clearer pricing for routine services to attract cost-conscious patients.

Consumer Behavior Changes:

Patients spending their own money tend to use healthcare services more judiciously, potentially reducing unnecessary tests or procedures. This could reduce routine care spending by an estimated 5-15%.

Increased Efficiency:

Transitioning routine care to HSAs or out-of-pocket payments could encourage innovation, such as more telemedicine or community health solutions, further reducing costs by 5-10%.

Total Estimated Savings: Combining these factors, systemic cost savings could range from 25-50% of routine care expenditures. For the total US healthcare system, this reform might yield 10-20% overall cost reductions, depending on how effectively competition and efficiency improvements are realized.

Excellent list! I was going to do something similar, so you saved me the work. I can refer people to this piece.